By Benedict De Meulemeester on 3/09/2014

Please find the Spanish article here.

Spanish (and Portuguese) energy prices are among the highest energy prices of Europe. Making a comparison between electricity prices is always difficult, as the exact level of pricing depends on many site-specific parameters. The graph below is based on real life examples of client sites with comparable consumption patterns. Underlying wholesale values have been calculated back to average Cal 13 prices during 2012. The data fit our general observations about price levels in Spain compared to other countries.

The table above is showing us two main issues regarding the electricity pricing in Spain:

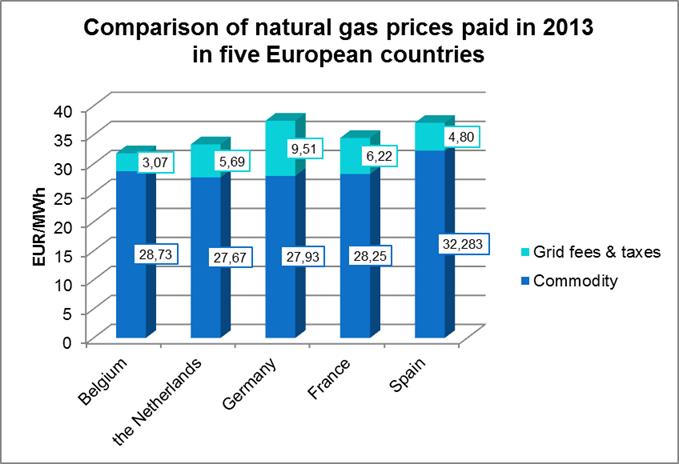

For natural gas, we cannot make the distinction between wholesale value and retail add-on, as Spanish natural gas is still billed according to old oil-indexed formulas and hasn’t switched to the more transparent Hub-pricing model of the other European markets. As you can see in the table below, this leads to higher prices, the second highest, just slightly below the German prices. But whereas in Germany, the problem is again situated in the regulated grid fees & taxes, in Spain what the suppliers are getting for their gas, the commodity price, is higher than in any other country.

Both electricity and natural gas markets are resulting in higher prices in Spain than in most other European countries. Spain has failed to implement features of energy market liberalization that have been a reality in other countries for years. Policy failures are the obvious culprit for this. But over the years, we have observed that some aspects of energy market organization fail to move forward in Spain, due to a lack of willingness by energy suppliers to develop new products, adapted to the new realities of the market. When we speak about this with energy suppliers, they also blame the Spanish energy consumers who – according to them – are not really demanding such new solutions. Based on these figures, we want to point out six priorities for reducing the costs of buying energy in Spain.

Spain and Portugal are one of the few regions left in Europe where the pre-dominant model for billing natural gas is still the oil-indexed model. The consequences in terms of pricing cannot be denied. You can see it in the table for 2013 above. In 2014, we see that Spanish gas prices have continued to increase. Spanish gas consumers easily pay more than 34 euro per MWh for commodity at this moment. This compares to 24 – 25 euro for forward prices in most other countries and spot prices that have dropped below 20 euro per MWh.

At first sight, the Iberian peninsular looks like the perfect place for implementing a virtual hub. It has no less than nine injection points, seven LNG terminals, a pipeline connection to Algeria and to France. Creating a virtual Hub means that the responsibility for shipping and balancing gas from any of these injection points to the end consumers is passed on to the grid operator. It’s not difficult to see how this would facilitate gas trading in Spain. However, despite much talk, nothing much has developed in terms of Hub activity in Spain. At some point, two different initiatives started to compete with each other, the Iberian Gas Hub from Bilbao and the OMI, which is the organizer of the Iberian electricity exchanges. From these initiatives, it is also clear that in Spain and Portugal the role of a Hub is not clearly understood. Both are focusing too much on the development of financial trading, whereas a Hub should focus on the physical aspects of trading and leave the organization of the deal-making itself through exchanges and/or OTC platforms to other market participants.

Iberian Gas Hub and OMI have now announced that they will join forces. Let’s hope these joint efforts will be more insightful as to the function of a Hub. Let’s also hope it gets the full support from the transport grid operators. Considering the declining demand for natural gas in Spain, the abundance of import infrastructure and the geographical position of its LNG terminals, en route from the Middle East to North-Western Europe, we are convinced that there is serious potential for lower gas prices. This would not just be good news for its gas consumers. As the marginal electricity MWh’s are often produced in gas-fired power stations, lower gas prices could benefit the power consumers as well.

Part of the high retail add-on for electricity in Spain is caused by the cost of complementary services, which has risen above 7 euro per MWh. With every power contract negotiation in Spain, you not only have to take a decision on the price level of the electricity itself. You also enter into complicated negotiations regarding the cost of complementary services. These are a sort of pass-through cost of fees that need to be paid by suppliers to the grid operators, a.o. for balancing the grid. Despite what many Spanish market participants think, there is nothing typically Spanish about these complementary services. Similar mechanisms exist in all the other countries as well. What is typically Spanish is that their cost has run up to unacceptably high levels.

It is true that the Spanish electricity grid has its particular challenges. The geographic spread of consumers and production plants is very wide, the market is isolated from the rest of Europe and, most importantly, Spain has a high percentage of wind and solar energy. The difference between a sunny, windy day and a cloudy quiet day in terms of plant commissioning requirements is indeed very big. But on the other hand, Spain has a production park that is well spread over the different technologies, which should lead to cost-efficient balancing. It specifically has a lot of hydro-electric capacity that should normally make it quite easy to balance the grid. We think that the high costs for complementary services in Spain should be seen as one of the many symptoms of the inability of its authorities of getting a grip on the regulatory framework. It should be fixed to lower the cost of consuming electricity in Spain.

What is even more annoying is that the system is based on an ad hoc calculation of costs incurred. This means that the cost for these complementary services is completely unpredictable and cannot be hedged. This leaves the consumer that wants to fix an electricity price on a forward basis with an uncomfortable choice that has to be made. Either he leaves the complementary services open, i.e. they will be billed at real, ad hoc cost, which means he is running the risk of unpredictable price increases. Or he fixes the complementary services. However, we have observed that suppliers will include a large risk premium in their fixing of the complementary services, which is logic, considering that they cannot be hedged.

If all other countries manage to get things like balancing costs regulated in such a way that it causes only minimal costs and no extra risks for end consumers, there is no reason why Spain couldn’t achieve this. This would lower the cost of buying energy in Spain and benefit the development of more retail market competition.

The first thing that strikes anyone when buying electricity in Spain is the six (or three) period billing system for commodity. Most other countries have switched to just two periods, peak and off-peak. In Germany, we often see simplified commodity billing with just one price per MWh, regardless of when it is consumed. But Spain has held on to the old billing systems of its regulated markets. We can understand that as far as grid fees are concerned, but we don’t understand it for commodity billing.

If you look at the wholesale market in Spain and Portugal (www.omip.pt), you’ll notice that it has also implemented the dual structure baseload – peakload that you find in all the other markets. The problem is that the six periods such as defined for calculating grid fees, doesn’t fit with these two products. This means that a supplier that is billing his client on a six-period basis, risks having a mismatch between what his client is paying him and what he is paying to the wholesale market in the two periods. To make up for this risk, Spanish suppliers will include risk premiums. This explains why the difference between wholesale and retail prices is higher in Spain than in other countries. If Spanish suppliers would bill end clients based on a peak and off-peak system or like in Germany, a single price based on a percentage of baseload and a percentage of peakload, the price they bill their end customers would reflect much better the price they pay for hedging the supply in the wholesale market. Thanks to that they could lower their risk premiums for covering the difference between the six and the two periods. It’s actually very simple. The more a retail contract reflects what a suppliers needs to do in the wholesale market, the lower the retail add-on. It’s surprising that Spanish suppliers haven’t discovered this potential for lowering their prices and increasing their market shares yet. End consumers should realize this potential for savings and lobby actively for getting contracts where the commodity price is no longer based on the six-period system.

In a liberalization process, there is a certain pattern according to which contracts offered to mid-sized and large end consumers develop. In a first phase, fixed prices are offered as an alternative to the old regulated tariffs. Next, multi-click or tranche model contracts are introduced to give these consumers the chance of managing the risk of fixing an energy price in a volatile commodity market. In a last phase, the market reaches maturity as these clicking contracts develop into more advanced hedging products.

It’s normal that next phase contracts are introduced for large consumers first and then gradually trickle down to the lower market segments. Moreover, many smaller consumers don’t need the more advanced contract types and can achieve their risk management goals with simple multi-click or tranche model contracts. However, in Spain, the development of more advanced contract types seems to have stalled. Spain is now, for example, the only Western-European country where a 10 GWh power consumer has a hard time getting offers allowing him to fix his price in different moments to manage the risk. In other cases, there is only one supplier willing to offer a flexible contract, putting the buyer in a very uncomfortable position. And in the gas market, the services for swapping floating oil-indexed prices to fixed prices are poor compared to what we were used to in other European markets when they were still predominantly oil-indexed.

Again, it is strange that Spanish energy suppliers don’t seem to realize that offering more advanced price hedging services can help them to expand their market share. At the same time, they are telling us that this is because Spanish consumers are not asking for them and just want to continue fixing their prices in one moment, even when they consume large quantities. The Spanish wholesale electricity price has fluctuated by more than 20% in the last three years. Spanish mid-sized consumers should get access to the contracts necessary to deal with that risk. And all consumers should get access to better price hedging services.

A few years ago, when we made international price comparisons, Spain stood out as a country with relatively low electricity prices. That position has been lost, and more and more international clients are starting to question this. As you can see in the table above high Spanish power prices are also due to the fact that its grid fees and taxes are among the highest in Europe. However, you can also see that the Spanish grid fees and taxes are in line with other countries that – like Spain - have been among the early adapters of renewable energy, such as Germany and Belgium. There are some reasons for having high grid fees and taxes for electricity in Spain. It should be remarked however, that in these countries energy-intensive businesses have more possibilities of getting exemptions than in Spain.

The problem of keeping a lid on grid fees & taxes in Spain, is closely related with an overall crisis regarding the regulation of energy markets. It is for example closely linked with the problem of the complementary services. The Spanish government has built up a historical debt in the utility sector by freezing end consumer prices in the past. It is trapped in a fierce dispute on how to pay back this debt. This puts the government in a difficult position when they have to negotiate tariffs with utilities. Solving this problem is necessary to keep the cost of energy for the end consumer under control.

Some of the problems cited above are linked to the fact that Spain and Portugal are an energy island. This is certainly the case for the electricity market. The geographical position of the Iberian peninsular is obviously the main cause for this, allowing for on-land connections with France only. But France in itself is well integrated into the North-West-European market and on top of that it has an abundance of nuclear power. It is therefore very strange that there is currently only 1.400 MW of interconnection available between Spain and France. As we have observed above, Spain’s electricity market has failed to develop market practices that are now commonplace in the rest of Europe. Better physical integration into the European market could get things moving.

As far as the gas market is concerned, Spain (and Portugal) is a strange case. Like electricity, cross-border connection with France is limited and the lack of North – South connection capacity within France is also problematic. But unlike electricity, natural gas can be transported by ship. With its seven LNG terminals lying on the shipping lanes from the Middle East (and Western Africa, and South-America) to North-West-Europe, you would expect the price surplus of Spain to North-West-European prices such as TTF to be quickly arbitraged away. But it’s not happening. Spanish gas suppliers quickly point at higher Asian and South-American prices as a reason for higher Spanish gas prices. But that doesn’t answer the following question: why is an LNG ship coming from Qatar sailing to the UK to sell gas over there when the price of the gas for the end consumer in Spain is at this moment more than 75% higher than in the UK?

The absence of a well-functioning Hub mechanism is a reason for that. But it’s not the only one. There are also failures in regulations and pricing mechanisms for key infrastructure such as LNG terminal slots, storage capacities or capacities on bottlenecks in the grid. Fixing the Spanish gas market will ask for more than just introducing a (well-designed) Hub. It will also necessitate the fixing of many other aspects of gas market regulation. Adding interconnection capacity to France could further improve the Spanish market situation. It should be remarked, however, that this should be combined with a reinforcement of the North to South gas pipelines within France. Doing so could connect Spain directly with the TTF market and create an interesting North-South corridor in the European gas grid. However, improving the conditions for LNG imports and exports in Spain should be the biggest priority as it could be a quicker and definitely less expensive solution.

As it has been explained before on this blog, it is widely disputed whether liberalization of energy markets leads to lower consumer prices. One thing is beyond doubt though, in a well-designed liberalization, the retail margin, what suppliers charge on top of the wholesale prices gradually decreases. We have observed this in many markets across Europe. Moreover, the service level in terms of price risk management normally increases. None of this has been observed in the Spanish market, showing that its liberalization process needs to be fixed. The six problems discussed in this blog article allow energy companies (suppliers and grid operators) to optimize their margins at the expense of the end consumers. Regulation flaws lead to windfall profits for energy companies that exploit them. Fixing these problems would stop the windfall, increasing the working capital available to Spanish industry. It could also lower prices paid by residential consumers, making more income disposable to the struggling Spanish households. It is clear that getting the Spanish energy market fixed could be a great support to its recovering economy. It should therefore be high on the list of its governments’ priorities.

One thing should be beyond doubt. Spain is not different. Of course, like in any other country, its market has its own characteristics, partly due to its geography and history. But the problems (or challenges) cited in this article have occurred in every single other European country as well. We don’t see any fundamental reason why Spain would be the only country in Europe that cannot solve them. Unfortunately, this ‘Spain is different’ mentality often keeps regulators, energy suppliers and even end clients from adopting solutions that have proven to be successful in other countries and could be just as successful in Spain. Success in Spain’s energy markets will be made by those that are willing to learn from the lessons learned in countries that have liberalized their markets more rapidly and more effectively. We as E&C are ready to use our experience across Europe and the US to help Spanish end consumers with that.