Working with big energy users in the midst of this energy transition, we sense the momentum for decarbonization. We have helped many of our clients realize their sustainability goals. Right now, one of our clients – let’s call them Client X – has just formulated their decarbonization targets and is in the process of negotiating PPA agreements. Always an exciting moment, but signing the agreement is by far the last step. This blog is aimed at demystifying the activities a company needs to consider once a PPA agreement is in the bag.

Signature of PPAs has an important impact on a company’s energy procurement activities in all its aspects. Namely: energy contracting, risk management and data management and financial controlling. We go into each of these aspects in more detail below.

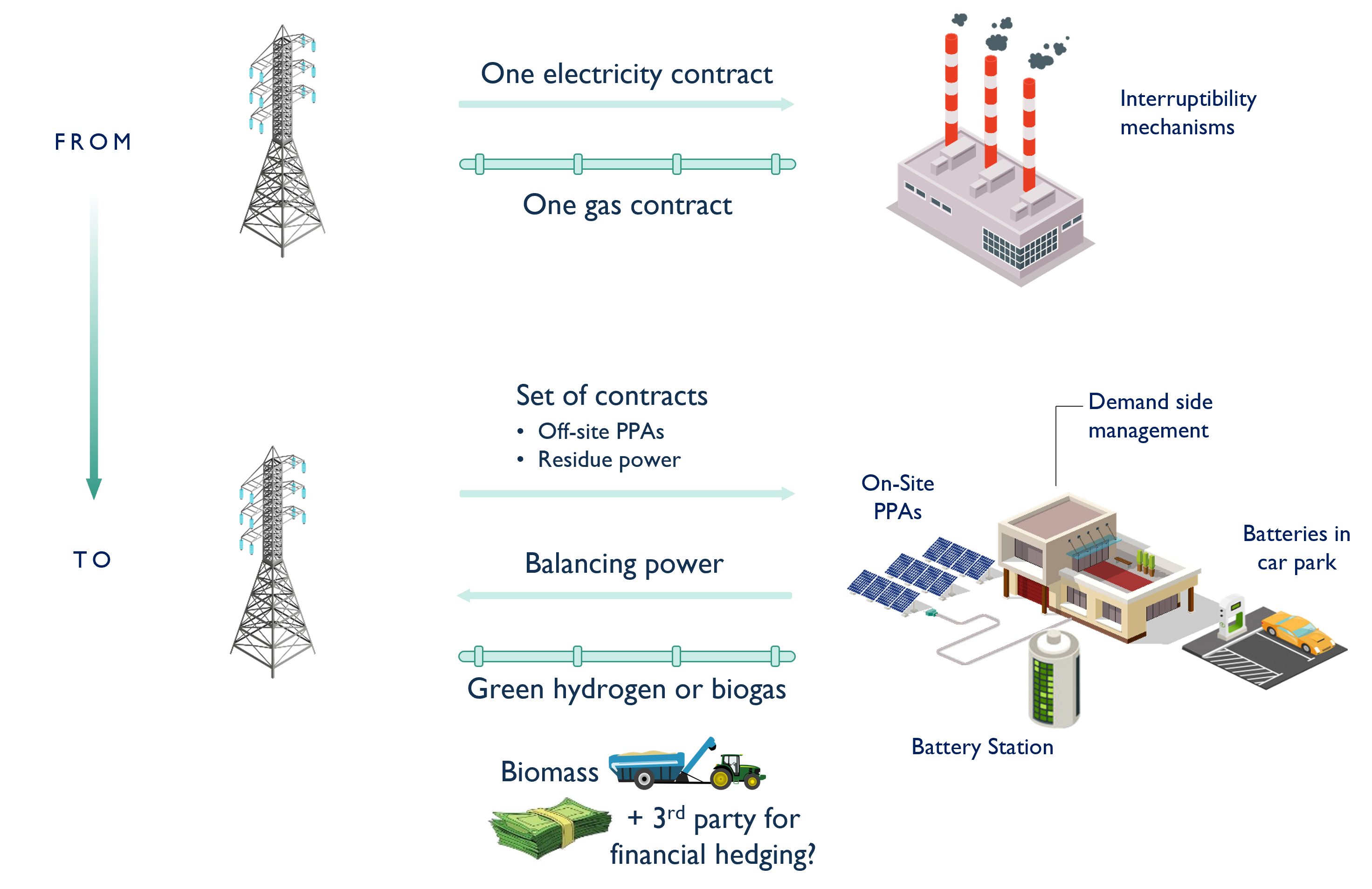

Energy contracting

Many clients have a relatively simple contract situation at this moment with all their sites in one country supplied through one electricity contract. Going through your corporate energy transition, you’ll find yourself in a much more complex contractual set-up:

- A set of on-site and off-site PPAs.

- Contracts for residual energy. As of the moment that you buy a large amount of energy (>25% of the annual volume) through (a) PPA(s) with an hourly spot regulation, it is advised to switch from the current contract model of buying flexible annual volume contracts hedged in percentages to contracts with an hourly spot price regulation. If the hedging is not done with a third party, then these contracts should include capacity band hedging services.

- Guarantees of Origin (GoOs) or other certificate purchases, combined with other contracts or not, but indispensable for proving the green character of the energy; PPA energy as well as residual energy. These might be included in underlying commodity contracts (we highly advise this for PPAs) or bought separately from them.

- Other energy transition elements such as batteries or demand-side-management will be covered by a specific contract.

- In case of large on-site generation or (battery) storage capacities, contracts for feeding energy into the grid will be necessary.

- When there are many different contracts, with different underlying price drivers in place, it’s often a good solution to contract a separate hedging service partner.

The factory of the future

Risk management

Risk management

In the current situation, Client X is subject to a relatively monolithic energy price risk:

- On the commodity part – in each country, the volatility risk of the underlying electricity and natural gas wholesale markets.

- On the non-commodity part – the regulatory risk of a government making (unexpected) changes to regulated tariffs for grid fees and taxes.

On the non-commodity part, Client X’s risk exposure remains largely the same since most of its incoming energy will keep flowing over the public grid. There might be some new risks associated with the injection of energy into the grid, in case of on-site production or usage of batteries. In the case that Client X engages in demand side management programmes, this will also entail specific regulatory risk.

The main change in terms of risk management needs, however, will be on the commodity side. Introducing PPAs in its supply mix will subject Client X to some completely new risks:

- Price risk: most PPAs come as fixed price contracts for the long-term. This means that such a contract can be considered as one massive hedge, which also means that this contract will subject Client X to a large price risk: the risk of that PPA ‘going out-of-the-money’, which would mean that Client X buys electricity – potentially even for a very long period – at a price that is higher than if it would have continued to buy that electricity from the grid. This risk of going-out-of-the-money is to be balanced with a strategic need for stable energy prices and decarbonizing the power supply with PPAs.

- Shape risk: most PPAs also come as a ‘pay-as-produced’ contracts. This means that Client X gets the electricity delivered when it’s produced. As we all know, for solar and wind power the production is highly irregular and unpredictable. As everything is cashed out on an hourly basis, this carves up Client X’s energy volume into three parts, each having their own risk management needs:

- Consumed and produced: the amount of electricity produced by the PPA is larger or equal to the amount of electricity consumed by Client X. This is the part of the energy for which you pay exactly the PPA price.

- Produced and not consumed: the amount of electricity produced by the PPA is larger than the amount of electricity consumed by Client X. The excess amounts of electricity will be sold at the hourly spot market price, which means that here you run the risk of having to sell this at low prices.

- Consumed and not produced: the amount of electricity produced by the PPA is smaller than the amount of electricity consumed by Client X. The extra electricity you need will have to be bought at the hourly spot price, which means that for this volume you run the risk of high spot prices.

This risk is not to be underestimated. E&C made some analysis for Client X where we matched a production pattern of a solar PPA in Spain for 100% of Client X’s volume in Spain with Client X’s Spanish consumption profile. The result was that only 26% of the total volume of energy transacted was produced and consumed volume. Which means that, contrary to the popular belief that PPAs lead to more price stability, in reality they lead to a larger exposure to spot market volatility. Moreover, this spot market volatility risk could be increased by the expansion of renewable energy that should result from the current boom in PPA requests from large corporates. This means that you could be structurally short in energy during hours when there is no wind and/or sun, hence exposed to high spot prices, and structurally long during hours when there is a lot of wind and/or sun, hence having to sell the excess electricity at low spot prices.

On top of that, buying 100% in a PPA is an illusion. First of all, the amount of electricity produced with windmills or solar panels over a year is never exactly the same. Secondly, entering into a 10-year or 15-year contract; it’s impossible to predict exactly what you will consume in that period. This means that your three volumes will also continuously change from year to year, where for some years you’ll be more tilted towards the long side, and other years you’ll be more on the short side.

- Basis risk: the large majority of PPAs are financially settled. This means that the power received through the PPA is sold at that hour’s spot price. Power consumed in the sites is bought back at the spot price. Often, the PPA production leg of this is set up as a swap arrangement where you receive the difference between your PPA price and the hourly spot price – but that makes no difference as to the final financial result. When a PPA is signed in the country where the energy will be consumed, the hourly spot price at which you sell the PPA electricity will be the same as the hourly spot price at which you buy the electricity that you consume. However, when you set-up cross-border PPAs, this will no longer be the case. This is exposing you to basis risk, the risk that the price at which you sell in the producing country is lower than the price at which you buy in the consuming country. This risk applies specifically to the volume that is produced and consumed. However, we should also mention that buying a large quantity of electricity in a cross-border PPA originating from only one producing country also means that you’re concentrating, hence enlarging your risk on the produced not consumed volume, in one country.

For all the risks cited above, risk management practices can be put in place to reduce the risk exposure. Some of those are up-front. This means that you diversify your PPA purchases over different PPAs to reduce the overall risk exposure. You can do this in a clever way: by applying spreading over technologies, geographically and in time. This will reduce the risk exposure but not completely eliminate it. Therefore, post-signature, risk management needs to be put in place. Client X is a budget risk client, meaning that the first goal of their energy procurement strategy is to stabilize energy costs over the long-term (see risk profile table below), these are in order of potential impact of the risk management practices that we recommend they put in place:

- Hedging of the volumes consumed/not produced and produced/not consumed. For consumed/not produced, this is a hedging strategy that is very similar to the current strategy for the total volume consumed. This means that to stabilize costs, hedges over multiple years are made when energy markets are low and in rising markets, stop loss triggers further incremental hedges to avoid that the energy cost from one year to another increases too much. For the volume produced/not consumed, a reverse version of this is to be put in place, where large volumes are hedged by selling futures when markets are high and then further volumes are hedged as markets start to drop. Such locking in of prices for volumes that are to be sold to a grid is something that E&C has been helping customers with for many years.

- Spread hedging. At a moment that the spread between a producing country and consuming countries are at a historically high level, the price can be locked in by combinations of selling and buying futures in the different countries. These are instruments that we have implemented for the hedging of multi-country gas contracts already for quite a long time.

- Re-indexing a fixed PPA price (for the produced and consumed volume) to the market. This can be done by selling futures when prices in the market where the electricity is produced start to fall. This instrument would get a high priority for a customer that is market risk oriented (see risk profile table below), meaning that such a client’s main goal of the energy procurement strategy is never having a price high above the market. For Client X, a choice is to be made here and this could be considered a further optimization possibility once the more advanced risk management practice as described in 1 and 2 above has been developed, rather than a necessity.

As you can see, setting up adequate risk management after PPAs have been signed will mean that more sophisticated hedging practices are to be put in place. This can be intimidating. However, any company in this position should consider that the complexity does not originate in the instruments to manage the risk, but in the more complex character of the risk to which it will be exposed when signing PPAs. The problem is not the seatbelt, it’s the risk of a car crash. Without appropriate risk management practices, Client X will completely lose control over its energy spend and be exposed to considerable spot market risks.

Data management and financial controlling

In the more complex procurement situation that will be created by signing PPAs, it will become impossible to read what you consume and what you pay from a single electricity bill. Determining consumption and cost for a site will demand the reconciliation of different invoices: the PPA invoice, the price at which power was sold to the grid, the price at which extra volumes were bought, and the hedges that were performed on different components. In a more advanced stage of the energy transition when more on-site production, batteries and/or demand side management programmes get blended into the mix, the number of parameters to be factored in will become even larger. At some point, this reconciliation will have to be made on an hourly level as contracts are cashed out over the spot market.

This data management aspect doesn’t ask for adaptations to the energy procurement strategy. However, we want to mention it here as it will be an important element of making the strategy work and to enable you to keep making good energy procurement decisions.

Want to understand what other decarbonization factors to consider?