By Benedict De Meulemeester on 16/06/2014

As of 2015, the UK will be the first European country to launch a capacity mechanism that aims at rewarding power plants for the MW’s they can produce. Similar plans for paying for MW’s are developed in other countries, including Belgium and Germany. We believe that there are serious reasons for concern as far as the end consumers are concerned because:

Why have capacity payments disappeared from energy pricing after liberalization?

Those among you that have been buying energy long enough to remember the regulated markets, will know that these prices contained important capacity components. The regulated tariffs paid for all elements of power supply: production, the supply itself and the grid utilization. As these tariffs were based on a dual structure of euro’s per kW (of capacity) and euro’s per MWh (of consumption), the single, monopolist utility received money (for the capacity payments) even when the consumption was very low.

When markets were liberalized, the different utility functions were split up. Grid utilization remained a (regionally) monopolistic market and continued to receive money based on a regulated tariff with the dual kW and MWh structure. That’s quite logical. Grid companies have high Capex and fixed costs, due to the high investments that are necessary for building the grids. A grid tariff with a high capacity component means that the grid companies continue to enjoy stable income, even when the number of MWh’s travelling over their infrastructure is going down sharply. The capacity-based payments are therefore creating a stable investment climate. This is precisely what the monopolistic utility deal is all about. The government gives the utility the certainty of clientele (the monopoly) and of stable income (fees independent of the consumption). The counter-side of that deal is the fact that the monopolistic utility is regulated. The government determines the tariffs and can make sure that this doesn’t lead to excessive profit-making by the monopolistic utilities.

The liberalization was all about introducing competition in the production and supply functions of the utilities, the so-called commodity part of the energy bill. Interestingly, the capacity components all but disappeared from commodity pricing. The whole market organized itself on a purely “per MWh” basis.

As far as the production or wholesale market is concerned, the powerful marginal cost pricing mechanism was introduced. Marginal cost pricing basically comes down to the following:

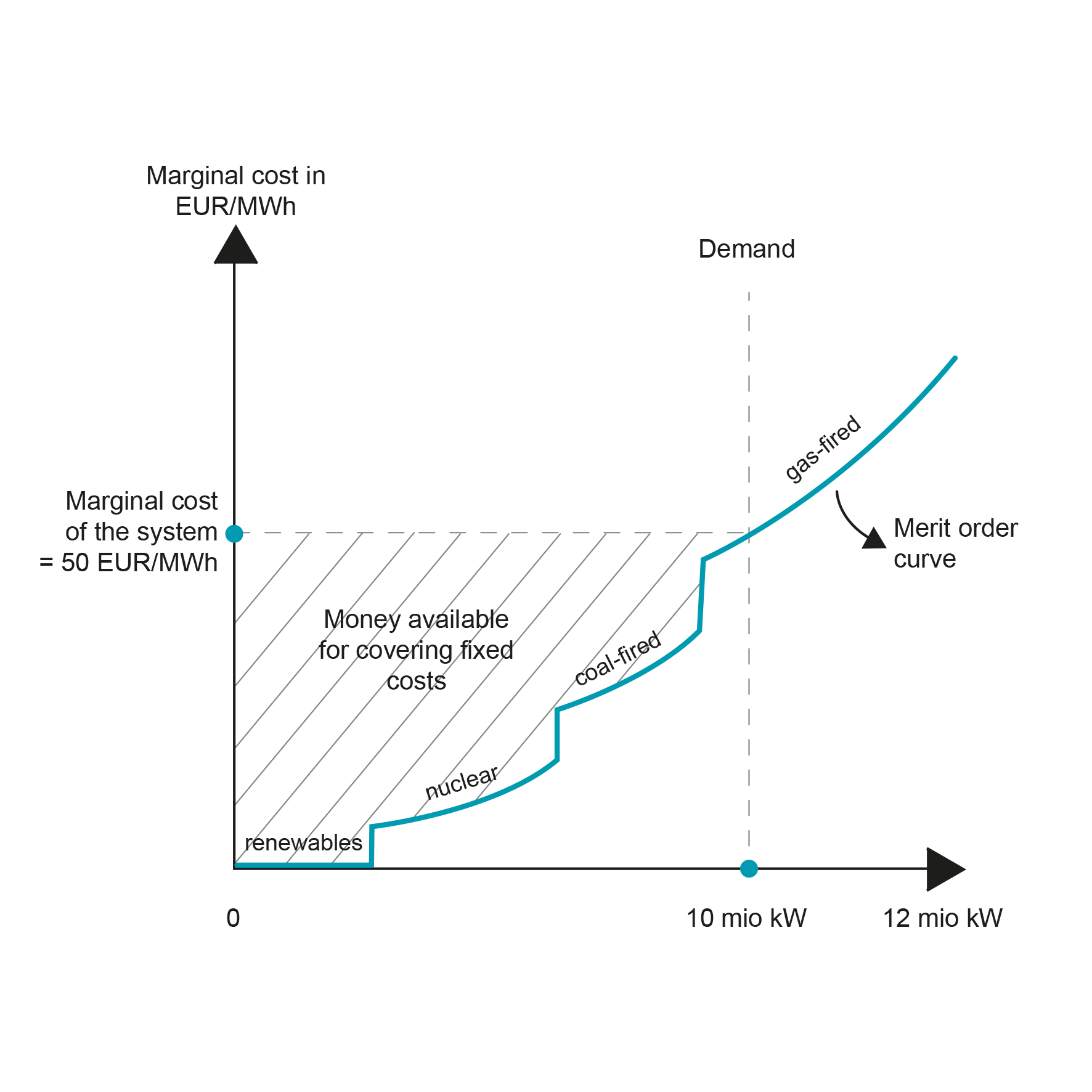

Figure 1: Marginal cost pricing for power supply

The exact size of the marginal cost is depending on a variety of parameters:

Marginal cost economics have installed themselves in wholesale electricity markets (both spot and forward) in a way that I consider to be of almost aesthetic beauty (I am aware how geeky this sounds). I’ll come back on that in a later blog article. One of the reasons that power markets have so readily embraced marginal cost economics is the overall cost structure of power plants. In an almost perfect way, the power plants with the lowest variable costs have the highest fixed costs and vice versa. Being on the left side of the merit order, high investment-cost power plants like renewables or nuclear, will always be “in the money”, meaning that they can produce and turn in positive cash-flow whenever they are capable (unless their combined supply is larger than the demand, something we’ve seen recently in Germany, resulting in negative spot prices). As these are the power plants with the highest capex, it also means that they have most euro’s available for paying back the investments. On the other side of the merit order, gas-fired power stations might have less hours during which they turn in money, but then they also have the lowest investment costs.

In the retail markets, payments of the commodity (or the deregulated) part of the electricity bill is in almost every country of Europe on an exclusively per MWh basis. Some incumbent suppliers have continued to include capacity components in their commodity pricing, but most have now given up. Either they buy the electricity on a per MWh basis in the wholesale market. Or they have an opportunity cost in euros per MWh when they source directly from their production – they could have sold it in the wholesale market at a price in euro per MWh. Therefore, selling it on to their retail market customers in euro per MWh is the simplest, most transparent and lowest risk option, which explains why it has been widely adopted.

Why are governments thinking about introducing the capacity payments again?

Marginal cost pricing is by its essence more volatile than pricing according to tariffs that contain fixed cost elements such as capacity components. They will drop lower and rise higher. Volatility makes everyone nervous, including governments. Let’s explain this with the example of Germany. In the last three years, the wholesale prices of electricity in Germany have dropped to a historically low level due to a combination of factors:

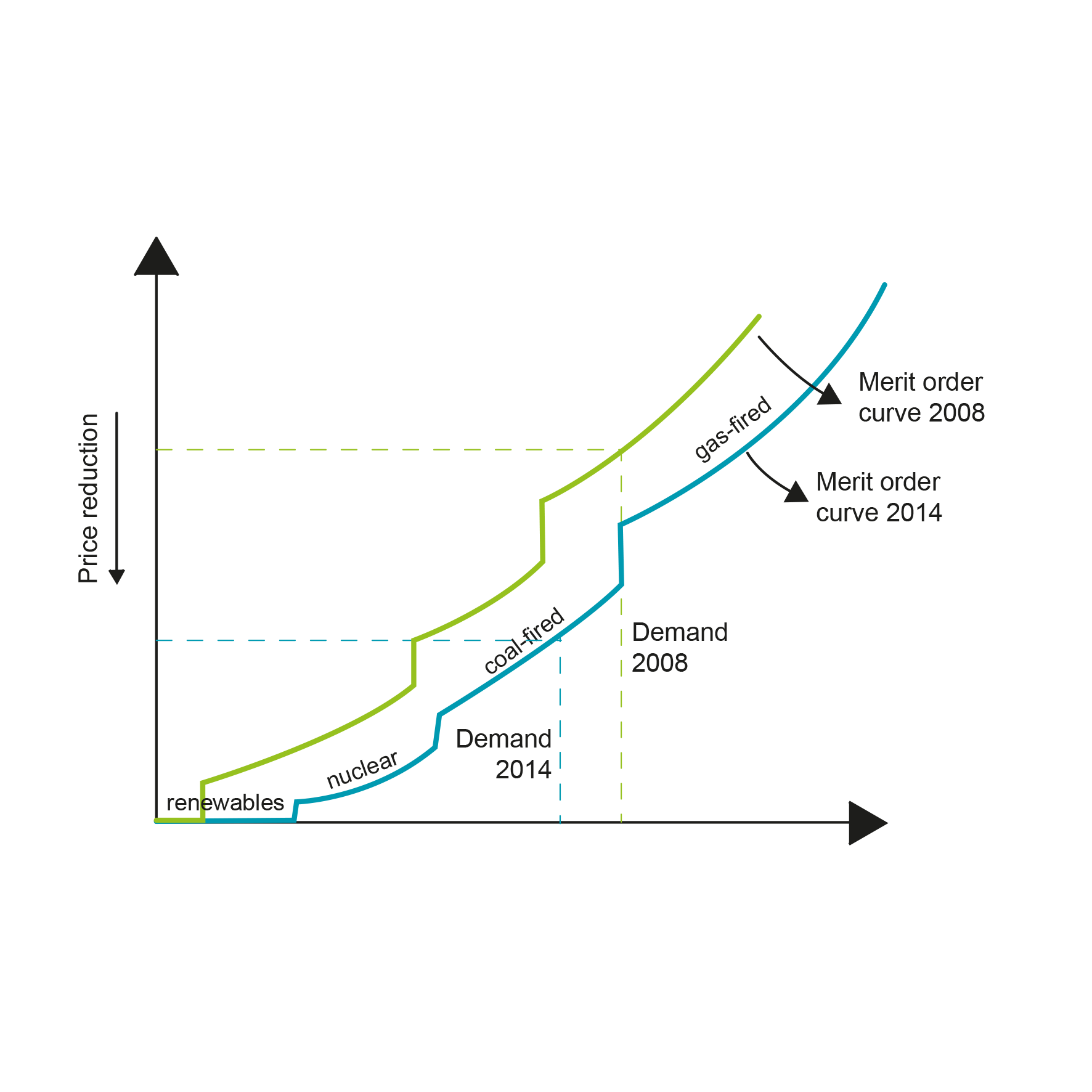

Fig. 2: German power cost reduction explained with marginal cost economics

Utilities are obviously complaining. They are not only seeing how assets are being pushed out of the money, the lower cash-flows on the assets in the money are also weighing on their profitability. The big losers are the gas-fired power stations. The combination of low coal, carbon and marginal prices with relatively high gas prices has pushed them far out of the money. These utilities are therefore lobbying actively for the installation of a capacity market or some other form of subsidizing power stations so that they continue to receive money even when they can’t sell their MWh’s because they are out of the money. Peter Terium, the CEO of large German utility RWE, for example, defends the introduction of a capacity markets with the words: “you don’t pay the firemen only when there is a fire” (Handelsblatt, 4th of March 2014).

The German Energy Minister Sigmar Gabriel seems to be hesitating whether he should give in to these calls for the creation of a capacity market or not. He calls for regional solutions rather than rolling it out on a national scale. Surprisingly, the UK, which was the first country to fully embrace energy market liberalization, is now also the first country heading for the introduction of a capacity market. The problem of the UK market is different from the problem in Germany. In the UK, policies to switch from coal- to gas-fired power generation, a nuclear phase-out and hesitant renewable energy policies have resulted in a production park with a very large share of gas-fired power generation (40%). You simply have a crowded right side of the curve of your merit order, meaning that too many power stations are out-of-the-money or just very slightly in-the-money. And as gas-fired power stations are (or were?) about the only ones for which it is (or was?) possible to obtain a permit, the government sees a need to intervene.

I find it very logical that energy companies are not happy with a situation of low profitability in which they struggle to pay back their investments. And giving its track record, I am not surprised that utilities call for the governments to help, to subsidize. Because in the end, whatever shape it takes, capacity payments are a subsidy. It’s the government organizing an extra source of income for the utilities. You can call it a capacity market, but it will never be a real or natural market. With a natural market I mean a market where an actual need for goods or services is economically arranged. As far as power is concerned, this natural market is the euro per MWh market. Just like that other artificial market, the carbon market, the capacity market will only exist because the government has decided that it should exist. If the government decides to cancel the capacity market, it will cease to exist, and we will still be having power. If the natural euro per MWh market for power ceases to exist tomorrow, then our lights will go out.

Now why have politicians been convinced of the need to create this artificial market for capacity? Even if there is no natural need for it, does it cater for some deeper need that markets cannot detect? The argument in favor of capacity payments which is used by utilities and politicians is that the market in euro per MWh isn’t giving enough incentives to invest in power plant capacity in a way that safeguards long term security of supply. Utilities naturally exaggerate this risk, using the powerful political argument of ‘the lights shutting down’. I don’t agree with that point of view, first of all because of personal experience. I’m working in the energy sector for 15 years and during that whole period I have heard about these threats of running out of power production capacity. The lights are still burning … Germany now produces large amounts of renewable energy. Industry insiders have always said that the intermittency issues of renewables would cause problems. Well, Germany has an extremely low outage rate of 15 minutes per power consumer per year, one of the lowest figures in the world. Power supply systems have proven to be much more flexible and capable of adapting to changing circumstances than most analysts estimate. Utilities, analysts and politicians acknowledge that there is no problem at this moment. It would be very strange if they did so, considering that the low commodity prices for electricity at this moment have a solid basis in excess supply capacities. So, what the capacity payments are supposed to solve is a problem of the future. I was hesitating to write ‘potential problem’ here. But apparently, the proponents of capacity markets are not. They make powerful projections about a future in which a power supply shortage is certain to occur. That’s forecasting, and I’m always very skeptical of that, especially when it’s done by someone who has a conflict of interest, which is clearly the case for an industry representative lobbying to get an extra source of income. In particular, I think that in this case the forecasts of looming shortages are colored by a combination of neglect and exaggeration of the following aspects:

What will capacity payments mean for the end consumers?

Very simple: the price of electricity will go up. The capacity payments will be compensated by adding an extra cost item to end consumers’ electricity bills. Some argue that this will be compensated by lower commodity (euro per MWh) prices. I don’t think so. If the capacity payments are handed out to existing power stations, nothing changes to the merit order curve. The power stations will still switch on and off at the same marginal prices as before, so nothing will change to the market price. The only thing that will happen is that utilities will benefit from a source of income that they didn’t have before. The capacity payments will simply be a transfer of cash from power consumers to power producers. Can such a transfer be justified at this moment in our economy? Yes, utilities are turning in less cash than before. But should their customers be victimized for that?

I can understand that for utilities the current situation isn’t nice. But they are not the first sector that goes through a phase of reduced profitability due to over-investment. That is the root cause of currently low prices. Utilities have over-invested in coal and gas-fired power capacity based on forecasts of a supply shortage that didn’t materialize. They have also invested a lot of money in renewable energy, raking in the subsidies that governments were giving for that. The marginal cost pricing made them win massive windfall profits on left of the curve assets in the 2005 – 2008 period when higher coal and gas prices caused marginal costs to go up to levels three times as high as what we currently see. Should the government step in immediately now that the wheel has spun around to the other side? Should they make the end consumer pay for that? Or should we rather say to the utility sector that it should accept normal entrepreneurial risk and don’t ask for a subsidy when their forecasts don’t materialize? Seeing assets turning in less money than expected is daily reality for businessmen in many different sectors. Why should the energy sector be an exception and get support from the government as soon as the weather turns bad on their investments? I see clients of mine in the food industry building large factories that in the best case will turn in just a few percentages of margin and assuming large risks in the soft commodity markets. They don’t ask for subsidies when they have a bad year.

For an end consumer, the conclusion is very simple. Mobilize your lobbying organization to avoid the introduction of capacity payments. At the same time, prepare yourself for its introduction by investigating you possibilities for reducing its impact with load management.

What are the alternatives?

From the above, it might be clear that as a policy option, the introduction of capacity payments should be carefully considered. Especially since I believe that there are alternatives:

Here’s my plan for an alternative to the introduction of capacity payments, a more cost-efficient and fairer way of reducing capacity shortage, avoiding unnecessary increases of energy prices for the consumers:

The end result could be a market where we produce ever lower amounts of power in renewable power stations and in gas-fired power stations at peak moments. If the grid in which this electricity is balanced is large enough and there is a good cushion of demand side adaptations, I don’t think that this will result in the sort of price peaks and blackouts that energy industry representatives predict. Introduction of capacity payments should be the solution of last resort, not the first thing we should think about. I know that if we introduce them only when the supply shortages manifest themselves, it will take some time for the extra capacity to be built. But I would rather risk two or three years of high peak prices and short blackout periods than risk an unnecessary and massive shift of money from power consumers to producers for solving a problem that in the end never materialized. We shouldn’t lightly risk creating a massive subsidy scheme that could result in over-capacity of unneeded gas-fired power stations.