By Benedict De Meulemeester on 6/12/2013

These complementary services are operations performed by the TSO to ensure a certain level of safety and quality on the energy delivery. Essentially, they are operating capacity reserves for active and reactive power, needed to maintain the technical balance between supply and demand.

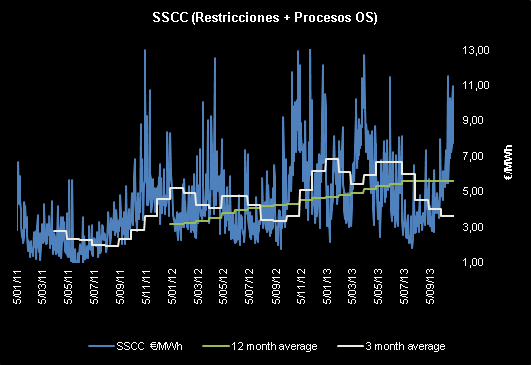

The following graph shows the evolution of these costs since early 2011.

During 2011 the average price of the SSCC was around 3 Euro per MWh. However, these costs began to rise above this average during 2012, with price levels as high as 13 Euro per MWh. The main problem does not come from price anomalies. It arises from the growth of the average cost as well as the increase of the volatility. We are currently facing an average price around 5,5 Euro per MWh and a price volatility between 1 and 13 Euro per MWh.

How does the SSCC price evolution affect us when we buy energy? Suppliers must forecast the cost of these services for both fixed price contracts and forward flexible contracts with indexed formulas. As there is no organized market for such services, nobody can hedge the risk. Therefore, the estimation is based on past values, future forecast and a risk premium.

In the situation mentioned above, it does not surprise me that some suppliers faced losses. Could anyone imagine that the SSCC costs would double? Probably not and the suppliers were not able to charge this increase to the clients.

Why did the complementary services boost? Which fundamentals drive their evolution?

There are two main drivers. On one hand, the percentage of "non-manageable" technologies in the energy mix: renewables and nuclear power production. Managing the supply-demand balance for the TSO becomes more difficult using this kind of technologies. As a consequence, the operating costs increase.

For instance, we saw Red Eléctrica (TSO) giving an order to disconnect the wind mills of the grid in April 2013. Moreover, it forced the nuclear plants to reduce 20% of their capacity. This resulted in massive costs. Managing the imbalances between offer and demand with gas-fired plants, on the other hand, is easier and cheaper. Remarkably, Spain is currently using only 10% of its gas-fired installed capacity. On top of that demand levels itself also affect the SSCC price, as these costs are shared by all the consumers. Subsequently, less demand results in a more expensive unit price.

From a procurement point of view, it is essential to assess the risk to which we are exposed. Afterwards, we should evaluate the alternatives the market is giving to manage it.

The first question to be asked, without taking into consideration the volatility of the forward market, is whether your company can bear a 3-4 Euro per MWh fluctuation in the energy bill. If the answer is negative, then the only option is to accept the Spanish market situation and pay the Premium.

If your strategy allows a certain price volatility, keeping these costs as "pass through" could be interesting. Doing so you can avoid you having to pay the risk premium, but does not avoid you paying future price swings. This option is only available if you have an flexible contract indexed to spot market or if you ask for a flexible forward market formula with the SSCC costs not fixed.

Nonetheless, is it possible taking further measures? Is there any other alternative? It is a surging debate in the market. Take into account that the estimation of these costs is based on historical data plus a risk premium. Therefore, it there should be a possibility of having a clause in the contract that enables the client to close the SSCC in the course of the contract duration and before the start of the energy delivery. Such a clause should be transparent and reliable. For instance, the client is able to close the SSCC, using the TSO’s 12 month moving average as a basis plus a risk premium negotiated beforehand.

If the suppliers are willing to give this option, calculating the risk and monitoring the evolution will be possible.

Does anyone accept the challenge?