By Benedict De Meulemeester on 16/08/2013

One of the more exciting aspects of a job as energy procurement consultant is that you get deeply involved in geopolitics. Elections in Iran, Russian post-Soviet policy or Arabian Spring Revolutions, we eagerly try to assess their impact on energy markets. What a nice job we have. Some conflict escalates on the other side of the planet, and the next day we are discussing the (possible) impact of that event on energy budgets with a client. It isn’t surprising that two of E&C’s consultants have studied political sciences. No, we are not just eating megabytes and megabytes of consumption data. Our life is more than just reading through the dull passages of energy contracts. Analyzing the impact of geopolitics on energy markets is the fun part. What makes for a better bedtime read than the books of Daniel Yergin, who dissects links between the world’s history and energy markets all the way back to the world wars. It wouldn’t be the first time that I make quite an impression during a reception when I explain how different the world would have looked if Hitler had reached Baku!

However, maybe because of the excitement involved, I’m convinced that geopolitics’ impact on energy markets is often exaggerated. This is certainly the case in the press, as journalists tend to be among the most passionate followers of geopolitics. They interpret any conflict anywhere in the world as having a price-increasing effect. I remember a spectacular example of that somewhere in the period before June 2008 when oil prices made their spectacular rally towards almost 150 dollars. Tensions in the Middle East, Nigeria or Venezuela were broadly cited every day as causes for this price escalation. On one day, North-Korea fired a missile and military conflict in Eastern Asia loomed. In the oil market comments of that day, the North-Korean tensions were broadly cited as a reason for rising oil prices … Hello? North-Korea is in an oil-consuming and not oil-producing part of the world. So, military conflict in Eastern Asia and its impact on the economy would most probably cause a decline in oil prices.

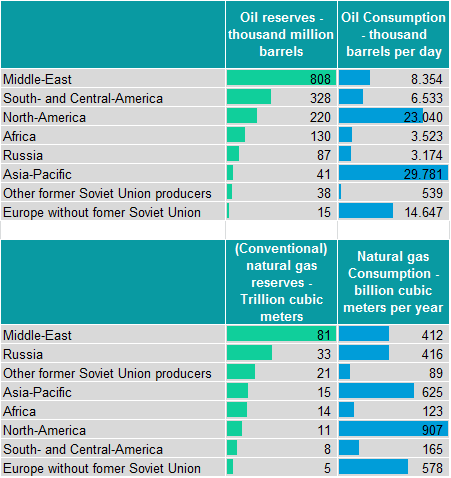

If we look at the oil and natural gas reserves versus energy consumption of our planet, we touch the fundamentals of this continuous linking of energy market analysis with geopolitical analysis.

Source: BP Statistical Review of 2012 – all data are for 2012

Consumption of oil and natural gas is highest in Europe, North-America and Asia, reserves are concentrated in the Middle East and the former Soviet Union. Add to these data four broad geopolitical conflicts:

The geopolitical connection becomes clear. Middle-Eastern countries, Russia or a country like Venezuela can exert political power that exceeds their pure political weight, thanks to their large reserves of oil and natural gas. Therefore, they don’t hesitate and distort the markets if it fits within their broader political goals. This is particularly worrying for Europe. Even if Europe consumes less than its North-American allies, it is extremely poor in resources. Its proximity and historical ties to mostly Russia and to a lesser extent the Middle East emphasize its vulnerability. This situation feeds worries over security of supply. In particular, it is feared that the producing countries will ‘wield the oil sword’, meaning that they cut oil and/or gas supplies in an attempt to support their geopolitical agenda’s. Every geopolitical conflict is then interpreted in the framework of this fear of the oil sword. Oil and gas traders have one eye on the Brent, NBP or TTF curve and another one on CNN or Al-Jazeera. They push up (forward) prices at the slightest sign of trouble.

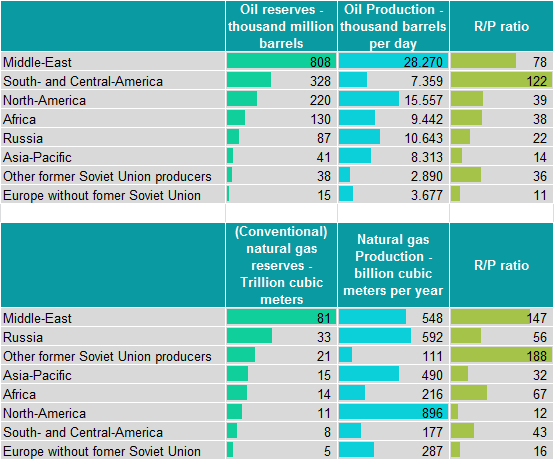

However, a totally different picture is drawn if you look at oil and gas reserves versus production figures:

Source: BP Statistical Review of 2012 – all data are for 2012

What we see in these data is that the regions with the largest reserves are not necessarily the largest producers. This is most clear in the so-called R/P ratio where total reserves are divided by annual production. These ratios are very low for natural gas in both Europe and North-America and to a lesser extent Asia-Pacific. They are also extremely low for oil in Europe and Asia-Pacific. Some will read these data as a sign of a looming energy crisis. But it can also be interpreted as a graph of missed opportunity. The Middle-East for example, is not exploiting the potential of its massive gas reserves. The situation is even worse for the gas under the soil in Kazakhstan, Turkmenistan, Uzbekistan and Azerbaijan.

The largest producer of natural gas in the world is the USA. In the last years, they have developed their shale gas reserves. Rather than tapping into the massive and easy-to-produce reserves in the Middle-East, they produce the more expensive shale gas at home. So, if the producing countries are indeed wielding the oil sword, the economic effect is a loss of market share and hence income. Hardly an effective policy, I would say. The Arab countries have experienced this when they cut oil supplies in the 1970’s. In the next decade, the US and Europe rapidly developed their off-shore reserves, leading to the rapid decline in oil R/P ratio that we see in the table above. This caused severe budget troubles in Saudi-Arabia in the 1980’s and 1990’s.

The same is true for recent Russian gas policy. The cutting of supplies through Ukraine during two winters in the last decade can be interpreted as an example of wielding the oil sword. Russians will – probably rightfully – respond that it was a justified attempt to sanction gas theft, but however you wish to interpret it, the effects are clear. European consumers grew anxious about Russia’s reliability as a supplier and this spurred alternative imports, mainly from Norway and Qatar. Compared to 2011, gas exports in Russia declined by 20,5 billion cubic meters in 2012. In Qatar they increased by 5,1 billion cubic meters and in Norway by 11,9. Russia is rapidly losing market share in its key exporting market, Europe.

The biggest story of missed opportunity definitely is Iran. The Islamic Republic has an R/P ratio for oil of almost 117 years, which is much higher than the Middle-East average of 78,1, with only war-ridden Iraq having a higher ratio. Iranian oil reserves are just 40% lower than those of its big regional rival Saudi-Arabia. Nevertheless, the Saudis produce more than three times more oil. And if you look at Iran’s situation in natural gas, the situation is even more disappointing. The R/P ratio for natural gas is a staggering 209 years. And, despite having the world’s largest reserves of natural gas for a single country, Iran is a net-importer of (Caspian) gas! Iran has been threatening the shutdown of the crucial Strait of Hormuz in the conflict over its nuclear projects. And it has always been a hawkish member of Opec. Well, this willingness to wield the oil sword hasn’t brought much benefit, on the contrary. If only Iran’s politicians had focused a bit more on developing its oil and gas industry instead of trying to use its massive reserves to get some political leverage.

The supporters of the Iranian regime will scream that this missed opportunity is due to Western sabotage policies. And the funny thing is that they are (partly) right. The Iran case is clearly showing that if geopolitics is effective, it is mostly when consuming countries are ‘attacking’. Cutting supplies has proven to be ineffective. But cutting consumption by imposing trade sanctions can be highly effective, as Iran’s case is clearly proving. The oil sword of the consuming countries seems to be stronger than the one wielded by the producing countries. Therefore, all this anxiousness in the markets about the countries with large reserves in the Middle East and Russia shutting down supplies is exaggerated. The oil sword hasn’t been wielded so very often and when it happened, it produced adverse effects.

Therefore, rather than looking at producing countries’ foreign policies, it would be much wiser to look at their internal policies. Are they, like Qatar or to a lesser extent Saudi-Arabia, creating an environment in which the oil and gas industry can prosper and develop the potential? Will the newly elected Iranian president Hassan Rouhani focus on that? And if we look at foreign policy, the question mainly is whether there is a willingness to soften the tone so that Western countries are less likely to apply trade sanctions.

This week, a client asked me whether the political showdown among Russia and the USA over Edward Snowden might not have a price-increasing effect on gas markets. In other words: will Russia wield the oil sword because of this conflict? Well, if they have the slightest apprehension of the real impact of geopolitics, they better not. And (warning: I tend to be slightly over-optimistic on such issues) there are some signals that this might be the case. The Kremlin seems to realize that its recent energy policies have caused loss of opportunity and apparently isn’t blind for Russia’s loss of market share (and highly needed export revenues) in Europe. The internal market for natural gas in Russia has been liberalized. I have no experience with buying gas in Russia, so I can’t really judge how effective this liberalization has been. However, in theory it could create the right conditions for gas reserves to be developed more effectively. And even more importantly, president Putin has indicated that he is willing to end Gazprom’s monopoly over Russian gas exports. He has approved a project by Novatek to export (liquefied) gas to China. A more liberal gas policy in Russia would be excellent news for the world’s gas markets, creating benefits for both Europe and Russia itself.