By Benedict De Meulemeester on 13/12/2012

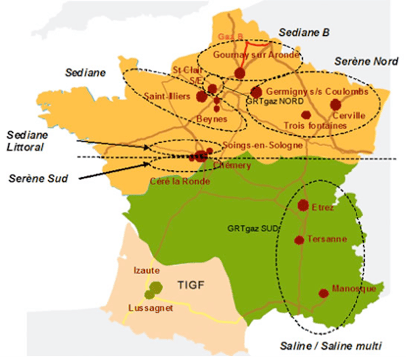

It has always been an oddity in centralist France, this part of the gas transportation grid called TIGF. It is situated in the South-West of the country and it is owned by Total and not by state-held gas firm GdF. Total has now decided to divest and sell its piece of French gas grid. Four bidders are selected: EdF, Enagas, AXA and CDC. Hold on, you might ask, did you say EdF and not GdF? Well indeed, GdF, owner of the rest of the transportation grid in France is not among the bidders. So the unification of France’s gas transportation grid will not happen.

One of the main flaws in European gas market liberalization is the lack of a North – South gas corridor. There is a pipeline link between the Netherlands and Italy, but so far, no extensive trading activity was seen due to failing capacity rights allocations. And Spain is a gas island, linked to the rest of Europe with just a small pipeline. Also, the lack of good links between France’s regional gas grids (PEG North, PEG South and TIGF) makes North-to-South gas competition difficult. Not unifying France’s gas transportation grid by having GdF at least bid for TIGF therefore looks like a missed chance at first sight. The lack of interconnection with Southern-Europe means that the key-consuming region in the North-West is not plugged directly into the gas fields of Northern-Africa. It also means that Spain’s many LNG import terminals, which due to the crisis have large spare capacities cannot be used to alleviate the broader European market. Organizing a better North-to-South gas market integration looks like a vital step in improving Europe’s diversity (hence: security) of supply.

The necessity of diversifying Europe’s gas supply has been emphasized by the recently announced takeover of Wingas shares by Gazprom. Wingas was a 50/50 joint venture between Wintershall, the oil and gas business of German chemistry giant BASF and Russian gas behemoth Gazprom. BASF has now ceded its shares to its Russian partner, getting access to upstream production assets in Russia in return. The acquisition of Wingas earmarks Gazprom’s continuining efforts to get hold of downstream assets in the European market. And this is not a small step. Wingas is a large gas supplier in Germany and has important positions in the Benelux, French and UK market and in Denmark, Austria and the Czech Republic. Gazprom is now completely owning one of the top ten European mid-stream gas companies. Getting control over Wingas is an important step in Gazprom’s strategy of acquiring a dominant position in the European gas market. Without entering into the geo-political speculations that always surround Gazprom’s business decisions, anyone with a heart for European gas market competition will agree that becoming to reliant on a single source of supply isn’t a good thing. With North-Sea gas production starting to decline and with increasing competition on the world’s LNG markets, extra supplies coming from the South of Europe could bring welcome relief.

(Just another remark on Gazprom’s acquisition of Wingas. Gazprom’s strategy of dominating Europe’s gas market doesn’t seem to be very successful until now. Gazprom seems to be losing rather than winning market share. The Russians’ stubborn resistance to the replacement of expensive oil-indexed gas pricing with the more fair and transparent pricing at Hub conditions is the main cause for this. Shortly after the announcement of the Wingas share deal, BASF announced that it signed a 100% Hub-indexed 4,5 bcm per year gas deal with Statoil. This is an important illustration of how Europe is turning its back on Gazprom and its oil-indexation fetish. But of course, if the Hubs can’t get access to supplies outside of Russia, Gazprom might prevail in the end.)

Returning to the South, it is very interesting to see Enagas, the owner of the Spanish gas grid bid for TIGF. If they would be successful, this could lead to a better interconnection of the Spanish and French gas markets. It could also mean that a cross-border gas grid and balancing zone comes near. We could consider this to be comparable to Gasunie’s attempt as of next year to extend the Dutch gas Hub TTF into Northern-Germany. Such cross-border gas grid operations are a very interesting developments towards an integrated European gas market. However, with so many things that are still to be fixed inside the Spanish market today, this paragraph might sound like day-dreaming, I realize. There remain issues to be solved with different odorization practices in France and Spain for example.

The fact that Electricité de France (EdF) is among the selected bidders confirms that the traditional French electricity producer continues to diversify. EdF wants to become a broader energy group by expanding its gas business. It is unclear to me in how far it can achieve this by going into the grid operation business. This seems to be based on the mistaken belief that owning parts of grids is helpful in extending market share. The experience of the past five years in Europe’s gas markets have shown that independent grids with easy access to their capacities are the best option for developing gas trading. It is also unclear how financial insitutions like AXA and CDC will contribute to solutions for Europe’s gas grid challenges.

Finally, by selling TIGF, Total is following a trend among IOC’s, Independent Oil Companies. These are retreating from downstream energy marketing to have more capital to invest in the increasingly expensive exploration and production activities where they are in fierce competition with NOC’s (National Oil Companies). Last week I was speaking to the country manager of a large IOC and he confirmed to me that his company had no intention at all to go into the retail gas business in Europe. Total is still offering gas to end clients in several European countries, among them obviously France. Could the sale of TIGF mark a broader retreat to the upstream activities?