By Benedict De Meulemeester on 3/02/2014

Topics: Energy Trading

Watch the interview with Benedict on this whitepaper

In many countries, energy markets seem to have reached a new level of maturity with buyers looking for new products that allow them to deploy more sophisticated price hedging techniques. One of those is the selling back to the market of forward positions that have been fixed before. This buying and selling of forwards is sometimes presented as a miracle solution that inevitably brings ultra-low energy prices. It is true that adding the selling of the forwards to the energy hedging toolbox opens up new possibilities. If well applied, it can produce good results. But we don’t see that every client that sells positions as well as buying them pays much better prices than clients that don’t do it. It is not a miracle solution. Moreover, we sometimes see it being deployed without appropriate energy risk management. And that sometimes leads to disaster rather than miracle. Before considering the selling of forward positions, it is key that an energy buyer understands the ins and outs of this sophisticated hedging technique to the last details. It’s not something that you can explain in a few simple sales slogans.

This hedging technique of buying ánd selling is often confused with portfolio management. If you enter a portfolio management agreement, it means that you mandate somebody outside your organization to take the price hedging decisions for you. That portfolio manager will probably want to use the full scale of hedging tools, including the selling of previously bought forwards. But portfolio management is possible without the selling technique. And you can deploy buying ánd selling without the help of a portfolio manager.

When I talk about this hedging technique of buying ánd selling, many clients debunk it as being too risky, too speculative. On the other hand, most traders find the fact that traditional multi-click or tranche model contracts don’t have the selling option too risky. Both are right. By having the possibility of selling a forward contract if markets start to fall after you’ve fixed your price, you can reduce the price risk. But because it is a more sophisticated hedging technique, the risk of something going wrong is higher. This means that buying ánd selling adds system risk to your energy procurement.

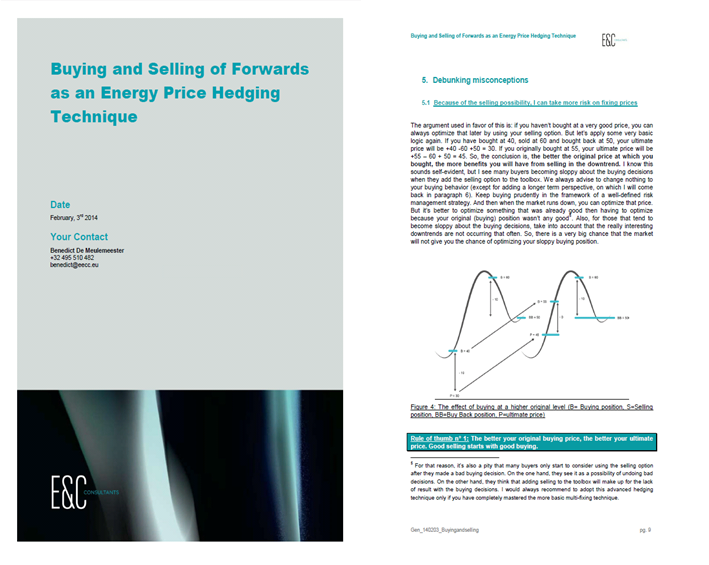

To deal with this higher risk of something going wrong when applying buying ánd selling of forwards, it is essential that you have a good understanding of how it works. The basic principle looks simple. You buy e.g. at 40, you sell that position at 60 and then buy it back at 50. Your ultimate price will be: +40 -50 +60 = 30. You have optimized your original position by the 10 (euro per MWh, e.g.) drop in the market. This is the simple + - + logic of applying buying ánd hedging. From it, you can derive two very simple rules for applying it successfully:

In theory, it looks dead simple, but in practice I see that even clients that have applied buying ánd selling for years make mistakes against this simple logic. For example, they get sloppy about their original buying positions, forgetting that the better your original price, the better your ultimate price. Or: they don’t want to sell at a price below the original buying price, losing valuable possibilities of improving the price in a downtrend. A third example of a misconception occurs when clients sell as soon as the price has risen above the original buying price, being too eager to cash in the ‘profits’ on the original position, but forgetting that they will have to buy back. To avoid such pitfalls, it is essential that everybody involved in the decision-making understand the basic + - + logic of this hedging tool.

Another misconception that I often hear is that people think that buying ánd selling is an energy procurement strategy in itself. It’s not a strategy, it’s a hedging tool. And how you apply that tool depends on your broader strategy that should be based on a thorough analysis of the type of risk that you’re exposed to in the volatile energy markets. Buying ánd selling can be used to optimize price results within the broader strategic goal of stabilizing energy budgets. But it can also be used by clients that have the opposite strategic goal of wanting to safeguard that they have competitive energy prices. Defining your risk limits and applying risk monitoring tools such as value-at-risk should help you in deploying buying ánd selling without excessive risk-taking.

If markets would move in straight lines, it would be very simple to be successful in buying ánd selling forwards. You would just buy everything if the straight line up starts and sell everything if the straight line down starts. But that’s not the reality of the markets. The price goes down for two days, then increases again, down again, etc. It’s this unpredictability of the markets that makes the application of hedging techniques so difficult. Some clients try to get around this by applying machine gun tactics, buying and selling at every first sign of an up-, resp. downtrend. That often results in big losses. I believe that it’s much safer to apply the piecemeal tactics, building up and down your positions in small steps, using your value-at-risk calculations to avoid excessive losses. I also recommend buyers to have patience. The real big gains are made in the big up- and downtrends. These don’t occur every year. If you trade too frantically in and out of every small intermediary trend, you’ll start piling up losses.

Operationally, the most important recommendation I can make is: apply the four eyes principle. Make sure there is at least one other person in your organization that completely understands the hedging technique to avoid disaster. Consultants such as E&C can also have an important role in deploying this sophisticated manner of hedging prices. I recommend to avoid black box solutions and to only use consultants that share all their information with you. Consultants should act as risk management consultants in the first place. The same is true with portfolio managers. Make sure that they are not taking excessive amounts of risk on your behalf by putting the necessary risk management practices in place.

Buying ánd selling of forwards is a powerful energy price hedging technique. It reduces the energy price risk by giving you the chance to reverse buying decisions. And it optimizes your chances of making really good prices as it allows you to benefit from downtrends in the market, and not only uptrends. However, it also adds a next level of complexity to your energy price hedging. And because of this complexity, things can go wrong. If you want to adopt this hedging technique, I recommend the following steps:

Good consultancy is based on an open and free exchange of knowledge. In this perspective, I have written a whitepaper on this topic of buying ánd selling of forwards as an energy price hedging technique. This blog article is a summary of that whitepaper.